Too many options. Conflicting rate claims. No clear sense of where to begin. If that sounds familiar, the real question is not simply which personal loan to choose, but which option best fits your financial situation and timeline.

Any meaningful personal loan comparison in Singapore usually starts with two practical considerations: whether you qualify for traditional bank financing, and how quickly you need the funds. Once those are clear, the rest of the comparison becomes much easier to evaluate.

For a broader introduction to personal loans in Singapore, Everything You Need to Know About Personal Loans in Singapore is the starting point. For a structural breakdown of how banks and licensed moneylenders are regulated differently, see Banks vs Licensed Moneylenders: Which is Better?.

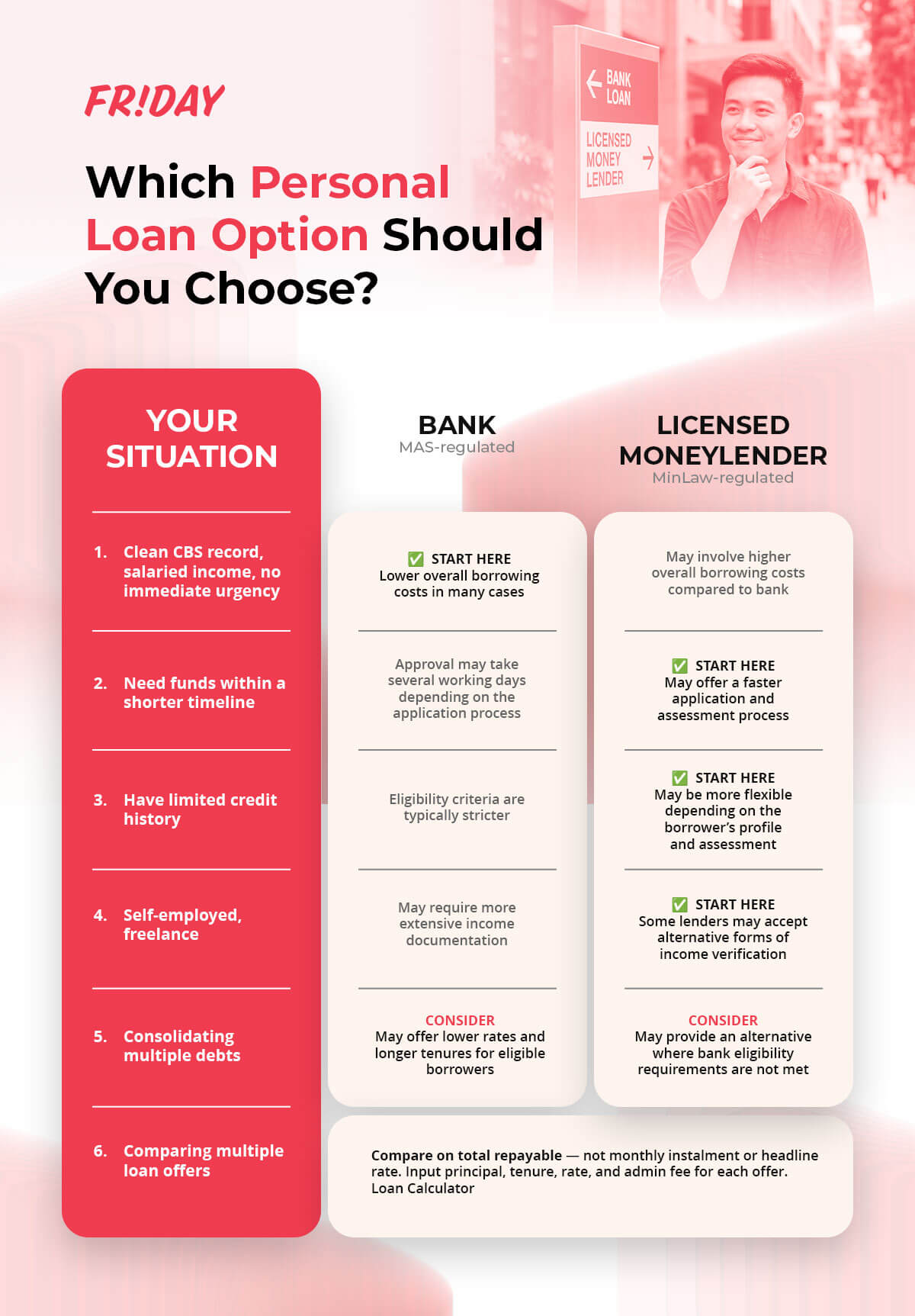

One of the most important questions in any personal loan comparison is not simply which lender offers the lowest rate, but which type of lender best matches your financial situation and borrowing needs. The table below provides a practical starting point by mapping common borrower scenarios to different lending options. Individual assessments and loan terms can still vary depending on the borrower’s profile and the lender’s criteria.

* Subject to individual credit assessment. Verify the lender's license before applying — banks via the MAS Financial Institutions Directory; licensed moneylenders via the Ministry of Law Registry of Moneylenders at rom.mlaw.gov.sg.

If you are unsure which category best fits your situation, it may help to start by reviewing the eligibility criteria before submitting an application. Check out: Understanding Eligibility Criteria for Personal Loans.

A structured personal loan comparison in Singapore covers seven factors. Here is what each one means and why it matters for your decision.

1. Interest rate. The headline rate — expressed as a percentage per month or per year — is the starting point. A monthly rate needs to be annualised to compare fairly across products. An annual rate quoted as "flat" is not the same as an EIR. Always confirm which type of rate is being quoted before using it in any comparison. See Understanding Personal Loan Interest Rates and Interest Rate Guide Singapore 2026 for a full explanation of how rates work in Singapore.

2. Administration fee. An upfront fee charged on the principal at the start of the loan. For licensed moneylenders, this is capped by the Ministry of Law at 10% of the principal. Some lenders refund a portion of the admin fee if you repay in full and on time — this is worth asking about, as it can meaningfully reduce the total cost for borrowers who repay as agreed.

3. Total repayment. The figure that matters most: principal plus all interest charged plus all fees. This is the only way to compare two loans on equal footing, regardless of how the rate is expressed or how the tenure differs.

4. Approval speed. If the funds are needed by a specific date, the timeline can matter just as much as the rate. Licensed moneylenders using MyInfo may return an indicative offer relatively quickly, while bank approvals can take several working days, particularly if additional documentation is required. It’s also helpful to distinguish between approval timing and when the funds are actually disbursed into your account. See How to Improve Your Chances of Getting Your Personal Loan Application Approved for a full breakdown of what affects approval timelines.

5. Eligibility criteria. The published criteria are a starting point; the actual assessment is more granular. Banks check your CBS (Credit Bureau Singapore) record while licensed moneylenders check the MLCB (Moneylenders Credit Bureau) — these are two separate systems that do not share data. Being declined by one lender does not necessarily mean another lender will reach the same decision, as different providers may use different assessment criteria and weighting factors. Reviewing your likely eligibility beforehand can help reduce unnecessary credit enquiries on your record. See Understanding Eligibility Criteria for Personal Loans for a detailed breakdown of what lenders assess.

6. Maximum loan amount. Licensed moneylender loans are capped at 6 times monthly income for borrowers earning at least S$20,000 a year, combined across all licensed moneylenders. In practice, the offer is usually below the regulatory ceiling — particularly for borrowers with limited credit history or existing debt.

7. Tenure. The repayment period determines your monthly instalment and your total interest cost. Longer tenure means a lower monthly payment but more interest paid overall. Shorter tenure means a higher monthly payment but less interest overall. Licensed moneylender loans commonly run 6 to 18 months. The right tenure is one that remains manageable even during a more financially demanding month — not simply the option that appears most affordable on paper.

Use this as a checklist when reviewing any loan offer. Offers are subject to the lender's individual credit assessment and terms.

Your priority determines which factors to weigh most heavily. The four scenarios below cover the most common situations borrowers face.

Scenario 1: Your priority is the lowest total cost.

You are salaried, your CBS record is clean, and timing is not urgent. You need S$15,000 over three years. Start with a bank. For borrowers who qualify, a bank personal loan is often the lowest-cost option — the lower EIR and longer tenure reduce total repayment compared to a moneylender loan. The trade-off is process time: approval takes several working days. That wait is worth it if total cost is the priority.

Scenario 2: You need fast approval.

Your CBS record has been recently affected, or you need funds for a time-sensitive obligation — a rental deposit, a medical bill, or a short-term cashflow gap. A licensed moneylender is a good starting point. Eligibility criteria are more permissive, and an indicative offer through a MyInfo-based application can typically come back relatively quickly. The cost is higher and the tenure shorter. Before committing, use the Loan Calculator to confirm the monthly instalment fits your actual budget.

Scenario 3: You have irregular income or a weaker credit profile.

You are self-employed, freelance, recently changed jobs, or do not have the multi-year income documentation typically required by banks. Licensed moneylenders may provide a more accessible alternative. Some lenders accept CPF contributions, payslips, or other forms of income verification, so it can be helpful to clarify the documentation requirements before applying. As with most lending products, broader eligibility criteria may come with higher borrowing costs compared to traditional bank financing. See Understanding Eligibility Criteria for Personal Loans for a detailed breakdown of what lender types accept.

Scenario 4: You want to compare actual repayment before deciding.

If you are comparing two or three loan offers with different rates, fees, and tenures, it helps to look beyond just the monthly instalment or headline rate when making a decision. Use the Loan Calculator to get the total repayable for each offer: input the principal, the tenure, the monthly rate, and the admin fee. The offer with the lowest total repayable — at a tenure you can sustain — is the one to choose.

Verify the license. For a bank: MAS Financial Institutions Directory at eservices.mas.gov.sg/fid. For a licensed moneylender: Ministry of Law Registry at rom.mlaw.gov.sg.

Get the EIR in writing. Rather than focusing only on the headline monthly or annual rate, compare the Effective Interest Rate (EIR), which provides a more consistent basis for comparing loan offers across lenders. If the EIR is not clearly disclosed before signing, it is worth seeking further clarification before proceeding.

Understand your eligibility before applying. A bank application typically triggers a CBS (Credit Bureau Singapore) enquiry, while a licensed moneylender application triggers an MLCB (Moneylenders Credit Bureau) enquiry. The two systems operate separately and do not share data directly. Multiple enquiries within a short period may still be taken into account by future lenders during their assessment process. Review Understanding Eligibility Criteria for Personal Loans and How to Improve Your Chances of Getting Your Personal Loan Application Approved before submitting.

Run the instalment against your actual budget. What you earn is not what you have available after rent, transport, household expenses, and regular commitments. The monthly instalment needs to fit what is genuinely left — not your gross income.

Read the agreement in full before you sign. Late-fee schedule, early-repayment terms, any bundled insurance conditions.

Ask what happens if you have a difficult month. Some lenders will renegotiate a repayment schedule if you raise it early. Others will not. Better to know this before you are in that situation.

Cost vs accessibility. Bank loans may offer a lower overall borrowing cost for applicants who meet the eligibility criteria, while licensed moneylender loans can provide an alternative for borrowers with different financial profiles or approval circumstances. Comparing across both categories is most meaningful when a borrower is realistically eligible for both; otherwise, the more practical comparison is usually between the options available within the category they can access.

Speed vs deliberation. A faster approval can be valuable when timing matters, but it is still a financial commitment worth reviewing carefully. Even within a tight timeline, taking some time to compare a few offers and read the loan agreements thoroughly is often worthwhile.

Tenure vs total cost. A longer tenure generally means lower monthly repayments but a higher total interest cost over time. A shorter tenure typically reduces the overall interest paid, though the monthly repayments will be higher. Neither option is inherently better — the right tenure is usually one that remains manageable even when a month does not go entirely as planned.

Friday Finance is a licensed moneylender on the Ministry of Law registry, operating as the consumer-lending brand of IFS Consumer Services Pte Ltd (license No. 85/2026), a wholly-owned subsidiary of SGX-listed IFS Capital Limited.

Interest rates and administration fees are tiered based on individual credit assessment, with stronger credit profiles generally qualifying for more favourable rates. In addition, 50% of the administration fee is refunded upon full and timely repayment. Loan tenures range from 6 to 18 months, with borrowing amounts of up to 6 times gross monthly income, subject to Ministry of Law limits and individual assessment.

Every unsecured personal loan also includes complimentary Personal Loan Protection insurance underwritten by ECICS Limited, another subsidiary of IFS Capital.

If a licensed moneylender fits your situation, view Friday Finance Personal Loan to see terms and eligibility.

A personal loan comparison in Singapore is most useful when it leads to a practical conclusion, not just a list of features or rates. For borrowers who qualify and are not working within a tight timeline, bank loans may offer the lowest overall borrowing cost in many cases. For those with irregular income, limited credit history, or more time-sensitive needs, licensed moneylenders may provide a more accessible alternative.

Before applying to either, verify the lender's license, get the EIR in writing, and use the Loan Calculator to confirm total repayment at a tenure your budget can sustain. Read Understanding Eligibility Criteria for Personal Loans and How to Improve Your Chances of Getting Your Personal Loan Application Approved before submitting a formal application.

For a full reference guide to personal loans in Singapore, see Everything You Need to Know About Personal Loans in Singapore. For a detailed structural comparison of banks and licensed moneylenders, see Banks vs Licensed Moneylenders: Which is Better?.

Which personal loan option should I choose in Singapore?

Start with eligibility. If you qualify at a bank — salaried income, clean CBS record, meets the minimum income threshold —a bank loan is often the lower-cost option for borrowers who qualify. If you do not qualify, or if you need funds within days, a licensed moneylender is the more realistic option. Once you know your category, compare on EIR and total repayable using the Loan Calculator — not on headline rate alone.

How do I know whether to apply at a bank or a licensed moneylender?

Start with eligibility. If you meet a bank's income and credit requirements, a bank loan is typically the lower-cost option. If you do not — thin CBS record, irregular income, recently changed employment — a licensed moneylender may be more accessible. For a full breakdown of how the two lender types differ structurally, see Banks vs Licensed Moneylenders: Which is Better?. For a detailed look at eligibility factors, see Understanding Eligibility Criteria for Personal Loans.

What does the admin fee actually cost me?

The admin fee is a one-time charge applied to the principal at the start of the loan — expressed as a percentage and, for licensed moneylenders, capped at 10% of the principal by the Ministry of Law. Some lenders refund a portion of this fee when you repay in full and on time. When comparing offers, ask about the fee percentage and any rebate terms, then factor both into your total repayment calculation. Use the Loan Calculator to model this accurately before applying.

How do I do a proper personal loan comparison in Singapore?

A proper personal loan comparison in Singapore covers total repayment, not just the monthly instalment or headline rate. Use the Loan Calculator: input the principal, the monthly interest rate, the tenure, and the admin fee for each offer. The total repayable is the number to compare. Two loans with different rates and tenures may cost nearly the same in total, or one may be significantly cheaper despite a higher headline rate.

Does applying for a personal loan affect my credit record?

Yes — although the type of credit enquiry depends on the lender. Banks typically review your CBS (Credit Bureau Singapore) record, while licensed moneylenders check the MLCB (Moneylenders Credit Bureau). The two systems operate separately and do not share data directly. Multiple enquiries within a short period on the same system may still be considered by future lenders during their assessment process. Reviewing your likely eligibility beforehand can help reduce unnecessary applications, particularly within the same category of lenders. See Understanding Eligibility Criteria for Personal Loans for a full explanation and How to Improve Your Chances of Getting Your Personal Loan Application Approved for guidance on improving your application before you submit.

Friday Finance is the consumer-lending brand of IFS Consumer Services Pte Ltd, a licensed moneylender (license No. 85/2026) regulated by the Registry of Moneylenders, Ministry of Law, Singapore. Loans are subject to credit assessment. The maximum loan quantum is set by the Ministry of Law and depends on the borrower's income and residency status. Interest rates and fees are subject to individual assessment. The Effective Interest Rate (EIR) may differ from the headline interest rate. Borrow responsibly.

The financial and regulatory information in this article is drawn from the following official sources. All figures are subject to change; readers should verify current information directly with the relevant authority.